Loyiso Bavuma

Loyiso Bavuma

Tax Attorney

Richan Schwellnus

Tax Associate

Both processes serve to prevent SARS from taxing the foreign income, with either a permanent, or temporary intention being the differentiating factor. It must be noted however, that both options attract the dreaded “exit tax”.

What Is “Exit Tax”?

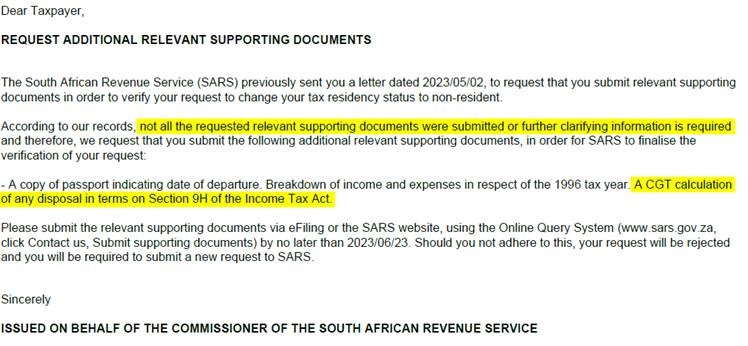

Without understanding the intricacies, South Africans abroad often try to avoid this exit tax by rolling the dice and not ceasing their tax residency. This is an immediate red flag, and when down on your luck, can open you up to the risk of a potential SARS’ audit. The audit is keenly focused on of the expat’s financial position after their departure from South Africa, however beyond that, there remains much confusion in the market as to exit tax and how/when it applies.

Many South African expats fear exit tax as they believe that SARS is waiting to tax all their assets when they arrive at OR Tambo airport; quite simply put, this is incorrect.

Exit is a once-off, deemed capital gains tax on specific worldwide assets of an outbound expat. This deemed CGT is basically a “fictitious sale”. From a practical standpoint, SARS claims tax on certain assets of an emigrant as if they had been sold the day before the expat ceased to be tax resident in South Africa; this is more often than not, the day before the expat leaves South Africa.

Which Assets Will Be Subject To “Exit Tax”?

Although not a closed list, the most common cases of where SARS will hold its hand out for the “exit tax”, are the below assets:

- Immovable property situated outside of South Africa;

- Krugerrands;

- Crypto assets;

- Global shares;

- Global unit trust investments; and

- Being a beneficiary and/or trustee of certain trusts where the taxpayer has a vested right.

The good news for South Africans proactively optimising their taxes through either the application of Double Tax Agreement or the Financial Emigration process, is that certain assets will not fall into the “exit tax” net. Excluded assets include immovable property in South Africa, cash, and retirement funds. There are also exemptions such as an annual R40,000 CGT exclusion which may be claimed.

Optimising Taxation with Offshore Employment

When the correct tax strategy is followed, South Africans abroad ceasing tax residency gain a first mover advantage, finding that following either the Double Tax Agreement or Financial Emigration process, may result in little, or in some instances, no, “exit tax” being due.

However, where dealt a hand of financial detriment now, ripping-off the “exit tax” band-aid will allow long term tax savings, actively preventing the double-taxation of future foreign income.

Be it your intention to formally emigrate, or simply spend some time abroad, correctly ceasing your South African tax residency will provide peace of mind; knowing you are compliant, should SARS’ audit radar ever come around.